Intellect Design Arena : The Fintech Enabler

Intellect Design Arena : The Fintech Enabler

Deep Dive into Business of Intellect Design Arena

Hi Folks,

Disruption ! Probably one of the most used word on Twitter and why shouldn't it be. We have seen major technological changes in last decade. Amazon has disrupted Brick and Mortar Stores, Uber disrupted taxi industry, Airbnb did the same thing for hospitality. We may question the profitability and sustainability of these individual companies with new competition arising each month, But if one thing's certain, Technology is changing the way we do business and the change is here to stay.

One of the safe pool to invest in this ever changing carnival is to invest in companies which enables this change. This strategy is also commonly known as Pick and Shovel, which came from the fact that people who sold picks and shovels to the gold miners during California gold rush of 1840s, made more money than the miners itself. Today, we are going to deep dive on business of Intellect Design Arena (IDA), which is enabling the digital transformation of Banking Industry.

“There are decades where nothing happens; and there are weeks where decades happen.” -Vladimir Ilyich Lenin

Digitization has already been a major theme since last few years, upon which COVID gave a shot in the arm. Along with the strong tailwinds, Intellect was already moving to a juncture where operating leverage is about to kick in. When both of these come together, one ought to take notice and study, so let's dive in.

Starting with a Quick Overview of Intellect as of last quarter and don’t forget to check valuation sheet in the last section.

Part 1 : Business Model and Industry Structure

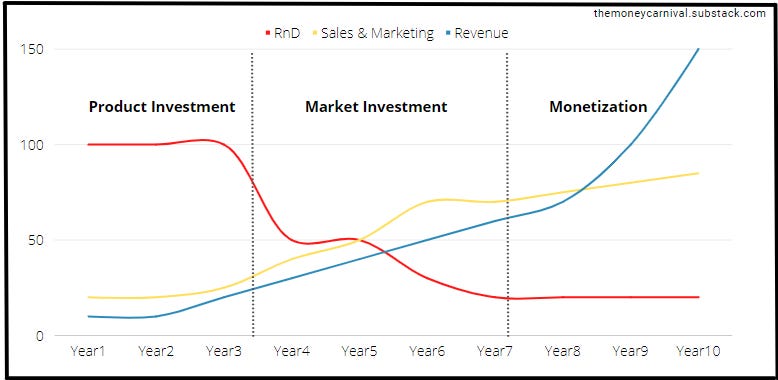

Intellect creates software products to facilitate different segments of Banking and Finance. Market for these products covers large spectrum of BFSI such as Consumer Banking, Transactional Banking, Risk and Treasury, Insurance. A typical product goes through few phases.

Stage 1-2 : Design and Development Phase - This stage includes investments in RnD and Sales and Marketing Costs with very low revenue coming out of it.

Stage 3 : Go-to Market and Acceptance Phase - This phase is about creating positioning in the market and spend on Sales and Marketing Costs to acquire customers. It could be inching towards breakeven at this point at the product level.

Stage 4-5 : Maturity and Monetization Phase - Once the product is positioned and got enough reference in the market, operating leverage starts kicking in as the incremental cost doesn't increase much while sales can grow exponentially. This is where Premium Pricing, Partnerships and Account Mining can take place.

This is how a lifecycle of typical successful product looks like. Once Monetization phase is reached, product becomes a cash generating machine with minimal incremental investment needed, which makes it a really strong business model. Needless to say, products do get extinct or lose their charm, if developers are unable to keep track of the changing demand requirements of end users; something that every investor should be careful about.

Intellect has several of such products in different phases of lifecycle which we'll talk about in next section. Before that, let's discuss the revenue model for a product company and demand side scenario

Sources of Revenue

There are two broad ways through which you call sell product in the market :

Licensing + AMC : Product Company charge a one time fee from client as a license cost of the software and then charge AMC (Annual Maintenance Charge) which typically costs about 20% of the license cost per year to continue using the product. There is a time gap due to implementation , customization and some milestones like UATs that ranges from 1-1.5 Years after licensing before AMC starts kicking in. Trend of AMC will also gives indication of license churn and customer satisfaction with product.

SaaS : Instead of One time licensing fee, software is provided as a subscription on pay per use / functionality basis. Consider this as taking loan instead of paying upfront cash, where we also cumulatively end up paying much more than the original cost. Hence LTV (Lifetime value of customer) increases with this model and gives predictability of revenues for a longer period of time.

Implementation and Customization : Since, banking products are complex and needs to be regulatory compliant, they need to be customized based on different regions and client's needs. This also includes training for in-house team and integration with client's other products. This is generally a low margin activity as it involves fixed human capital for certain period on particular client, however, Intellect is reducing the implementation period over time because of increased efficiencies as company gets similar deals in one region and also partnering / outsourcing the implementation work to IT services companies.

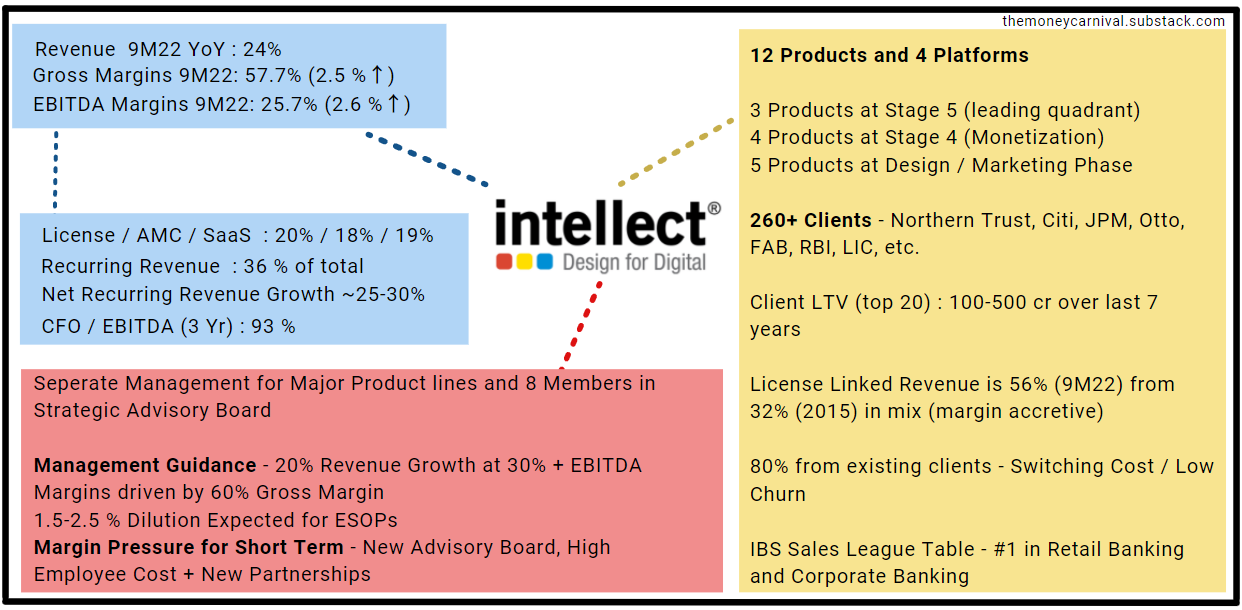

(ARR) Recurring Revenues : SaaS + AMC has increased from 18% to 36% of the total revenues. Growth of recurring revenues shows the improving quality of business which will eventually lead to operating leverage / better valuations of business driven by sustainable and predictive free cash flows for a long period of time.

Demand Side Scenario

There are several factors leading to tailwinds for Software Product Companies:

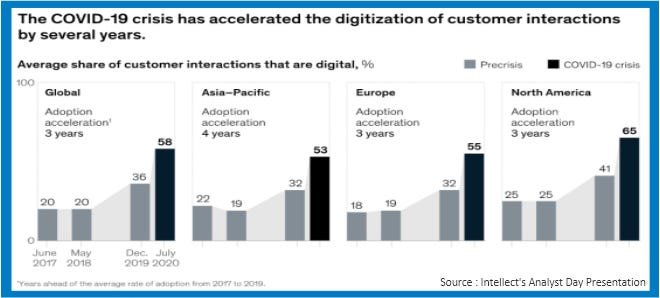

Digitization : Since last few years, Banks have started moving towards digitization along different functions to provide better customer experience. $2.4 bn of incremental digital application spend by Financial Institutions is projected by FY25

Shift to Buy vs Build : Covid 19 has pushed acceleration of digitization and banks are looking for quick turnaround which leads them to focus more on buying products rather than building in house.

Increased Cloud Adoption : As we've discussed in previous blog, SaaS is getting more traction since it's a win win model for both parties. Corporations can try and use different products at a fraction of cost while product companies get higher LTV with more predictability of revenues. SaaS Cloud spend is expected to grow to be 25% of all on-prem app spend.

Part 2 : Products, Use Cases and Competition

Before we discuss about the products, lets clear out a few keywords that come here and there in company's product discussion

Contextual Banking - Providing Actionable Insights through audio / visual medium (with help of AI / ML). for e.g. in Intellect’s context, this is used with DTB Platform to manage firms’ cash and trade that leverages ML and predictive analytics, which helps banks Up Sell and cross sell by providing clients with content aware recommendations on best next action. In following video, this has been explained more simply.

Open Banking - Open banking is a banking practice that provides third-party financial service providers open access to consumer banking, transaction, and other financial data from banks and non-bank financial institutions through the use of application programming interfaces (APIs). For e.g. You must have seen apps that fetch data from your different banks providing budgeting, savings portfolios, overview of finances, etc.

MACH - Microservices, API First, Cloud Native, Headless Architecture

Microservices - Also referred as ‘Composable Program‘ - Product is built in such a way that Individual pieces of business functionality that are independently developed, deployed, managed and can be scaled individually.

If you’re more curious, below video is one of the best video I’ve seen on microservices 101.

API First - How do we get different microservices to interact with each other? APIs. APIs are the interface which will help fetch data / provide data to other programs / applications / services.

Cloud Native - Software-as-a-Service that leverages the full capabilities of the cloud, beyond storage and hosting, including elastic scaling of highly available resources. Functionality is updated manually, eliminating the need for upgrade management.

Headless - It’s all about user experience. We want to see our applications in multiple devices - Laptops, Tablets, Mobile, IoT device, VR sets, smartwatches, etc. The front-end user experience is completely decoupled from the back-end logic, allowing for complete design freedom in creating the user interface and for connecting to other channels and devices

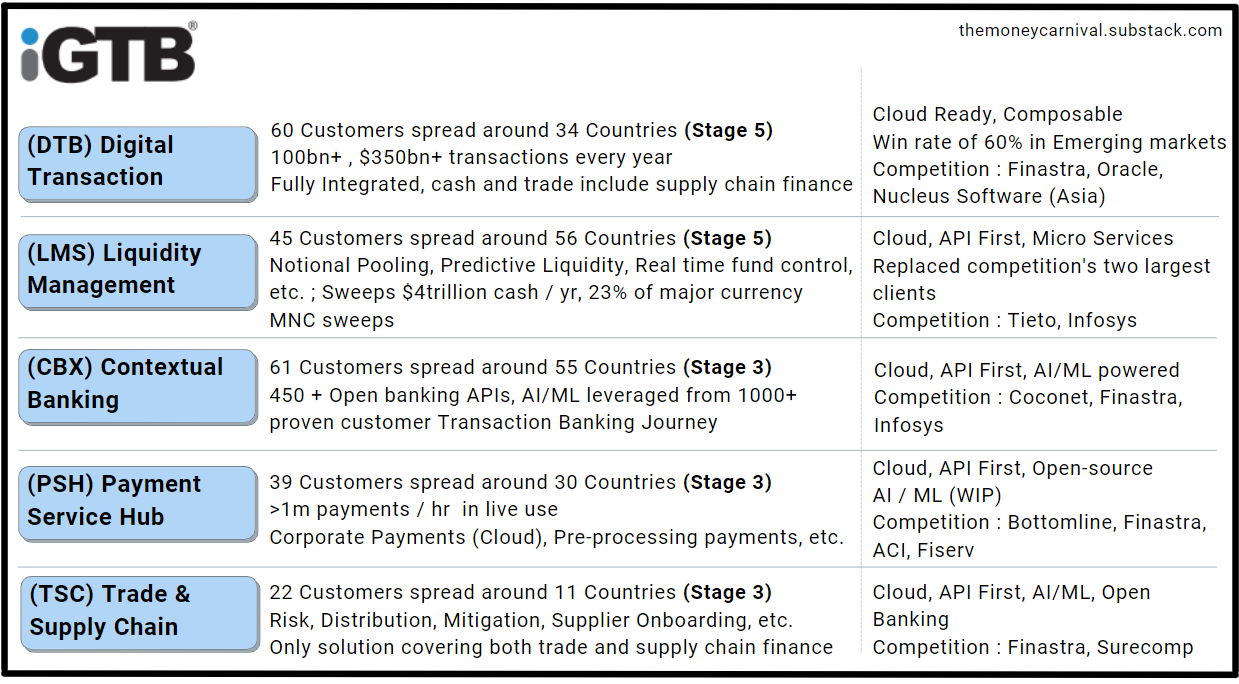

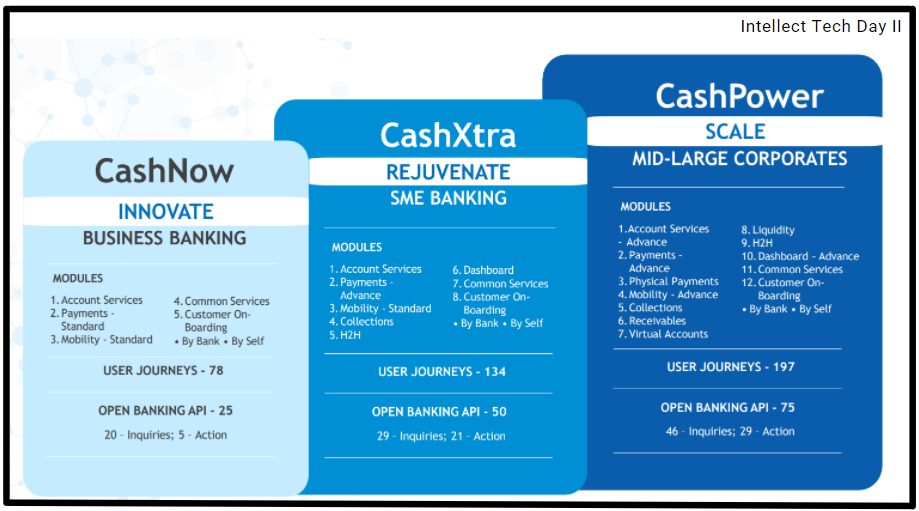

iGTB : Global Transaction Banking

IBS Intelligence : #1 in transaction banking solution in world (2 years in row) ; Gartner : #1 for full score on interactive open banking channel capabilities

15 of the top 50 global banks clients includes JP Morgan, Citi, HSBC, Santander, Barc, Llyods Bank, Mizuho

Few of the notable clients for DTB in India are HDFC, IDFC, Société General

DTB and LMS under iGTB are the products that has reached critical mass i.e. Good Reference, Premium Pricing, Large Client Base.

Payments and Trade Solutions are expected to reach up a scale in coming year.

Total 92 Customers with average 2.7 Products per Customer. Aim to reach 150 customers at 4 Products per Customers.

Implementation has been faster around 10-25 weeks.

Platform based on above products : Cloud Cash Power '22

Technology to claim better positioning in Market : iTurmeric

iTurmeric works as an integrator to connect Intellect products with 12 other leading core banking systems making it as value added service which helps business win more deals.

iGCB : Global Consumer Banking

As name suggest, these products help in consumer / retail banking, for which Intellect's addressable market - $10.8 bn, growing at CAGR of 10%

Focus on strategy towards Europe

Quantum Central Banking Product has reached scale under iGCB but TAM is only 100 banks across world.

Next products to reach scale for Intellect are expected to be Digital Core and Lending.

Found whitespace in Credit. Launched Platform iKredit 360 in July 2021.

Digital Customer Onboarding segment is gaining a lot of traction.

There is another product - for Digital Cards, which is in process.

Following is the demo of Digital Bank Use Case shown during Tech Day II.

Timestamped Link : https://youtu.be/cnyZ-LUk5_k?t=6636

Platform based on above products : iKredit360

https://vimeo.com/556481876?embedded=true&source=vimeo_logo&owner=106691480

iKredit360 : Built with Composable tech. ,the platform has been designed with a Global approach, exclusively for European financial institutions, ecommerce players and Non-banking Financial institutions.

Ecommerce players, financial institutions and NBFIs in Europe can leverage this platform to curate credit experiences for their consumer, merchants and channels-partners. With its ability to converge multiple elements such as internal and external systems, financial products, credit lifecycle and fintechs, empowers financial institutions to expand and extend their credit experiences to become the primary engagement point for their customers.

iSEEC

These products are mainly focused on improving the underwriting process at each step however, the technology has use cases beyond Insurance industry too.

IDX : Data Extraction Technology : Classification of documents, Extraction of data with high accuracies in minutes, validation and enrichment, verification (refining through AI as the data grows)

Reached accuracy of 98% with one of the clients in extraction

One of the use case is Magic Aadhar which helps in validation of Aadhar no. against UIDAI API

eKYC regulatory checks against Govt. mandates for LIC

Data Extraction also has use cases in other industries like Healthcare, Manufacturing, Retail

Speed up process of underwriting , data cleaning, quick insights of data

All 3 Products - Magic Submission, Risk Analyst, Xponent are cloud native SaaS Products.

Intellect’s addressable market considered to be around $100m

Global Commercial Insurance market - projected to grow to $1.61 trillion by 2030, 9.7% CAGR by 2030

iRTM (Risk, Treasury Markets) & iWealth

This segment is in development and go-to market phase

Planning to monetize in FY22-23

Capital Cube (Treasury) : Functionalities of integrated front to back treasury, contextual asset liability management, portfolio risk analytics and self service FX office for bank’s corporate customers. This is a cloud based low code interface with contextual UI/UX. 50+ Treasury clients across globe using this solution.

Capital Sigma (Risk) : Digital Platform that supports high STP, Variety of asset classes and market segments. It minimizes post-trade operational risk and increases operational efficiency by digitizing asset servicing functions across front to back offices, access to real-time information for investors, compliance reports for regulators and portfolio performance and analytics for better decision making.

Wealth Qube : A composable wealth management solution for private banks, wealth management businesses, advisory firms, family offices, broker-dealers, and independent financial advisers, allowing straight-through processing from front to back office.

Part 3 : Financial Analysis

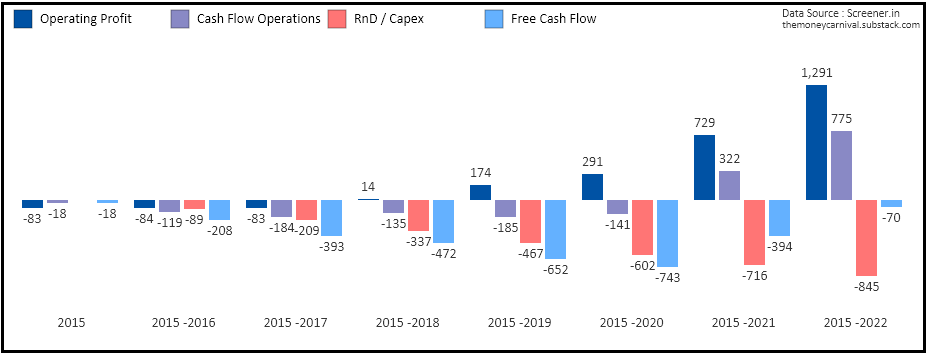

Cash Flows

As products are reaching scale, we can see incremental increase in cashflows surpassing the increase in RnD Costs. RnD Costs are growing at slower pace, with increase in Cash Flow from Operations and hence free cash flows.

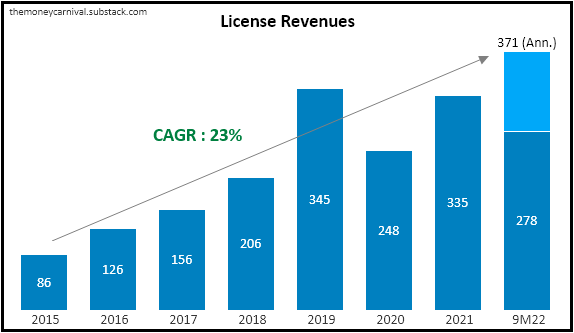

License Revenues

One of the health metric to track for a product company is to track license growth, which shows that there is customer confidence and satisfaction in product. Growth in license revenues has been consistent over the year. A portion of revenue that used to come as License is also being translated as SaaS because of evolving technological ecosystem.

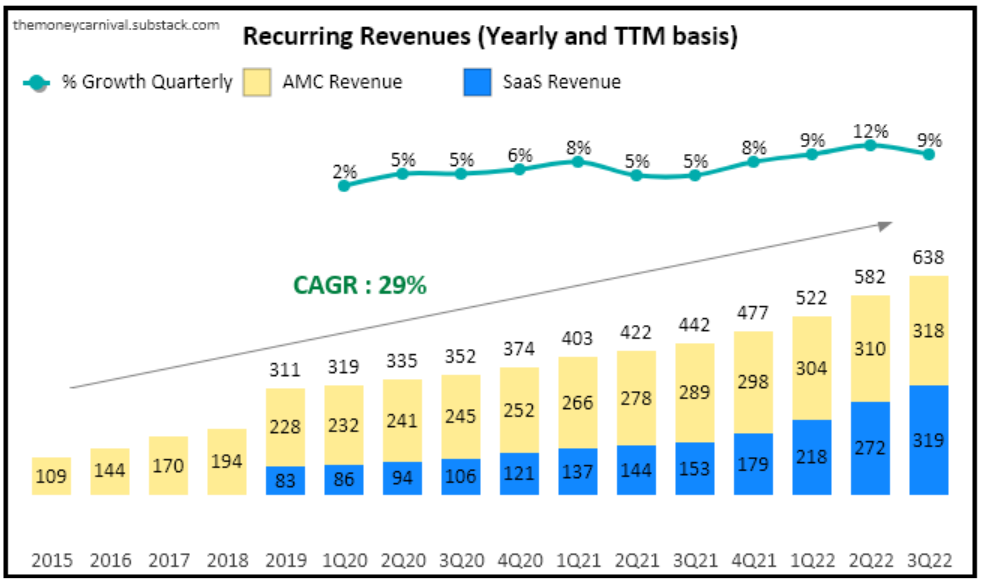

AMC & SaaS Revenues

As we already discussed, AMC and SaaS revenues are recurring revenues for long term with high margins and high growth in their revenues is one of the major thesis for intellect. Since these are mostly annual or monthly revenues for different account values, it's best to track them on TTM Quarterly basis.

There are two major components to Cost

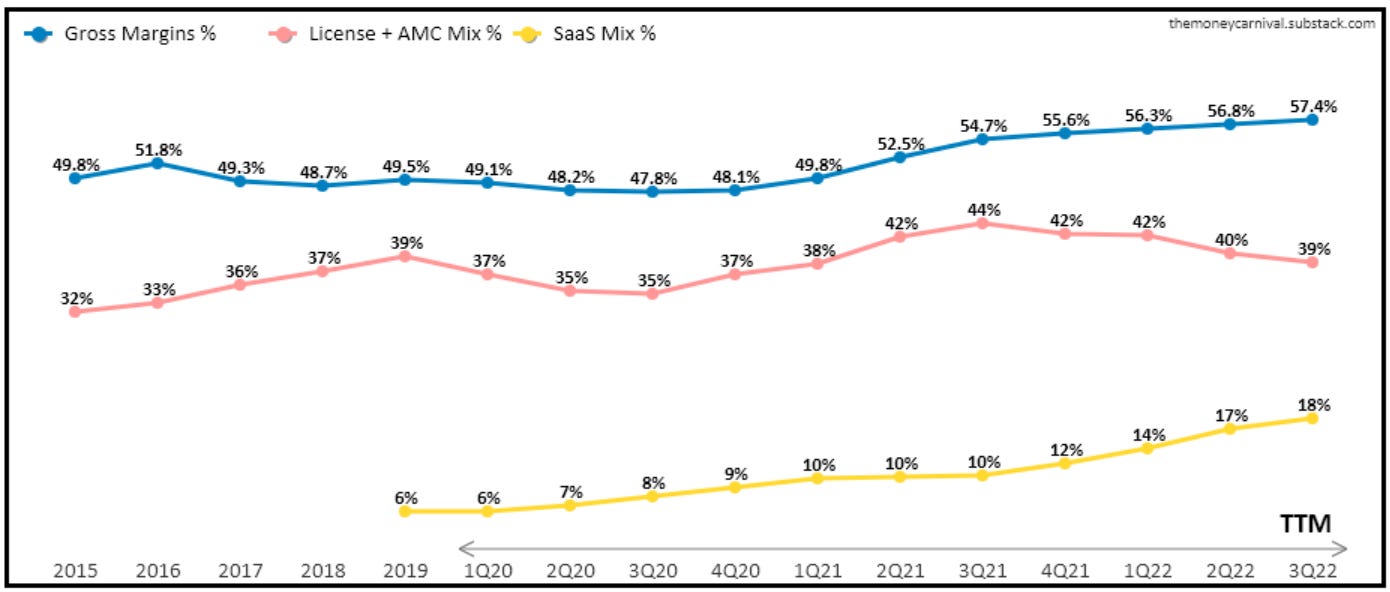

Software Development Expenses and Gross Margins

Software development cost determines the gross margin for business. It has been in a range of 49-50% for a long time as majority of the products were in Stage 3-4 Phase. As they move more products to Stage 5 where they can set premium pricing and acquiring more customers, and hence increasing the ratio of License Linked Revenue in the mix, they'll be able to increase the gross margins.

Another thing to note here is even though contribution of license linked revenue has increased in 2019 and 2020 but it was mostly due to SaaS Revenues, which doesn't absorb all the cost like the upfront license revenues, causing gross margins to stay in a range.

From TTM 2Q21, license linked revenue is growing steadily and hence increasing the gross margins%. As mentioned by Arun Jain in one of con-call, Largest contributing products enjoy gross margins of 60%+ in this business and as products starts getting monetized, we can expect to reach gross margins of 60%+ in a year or two.

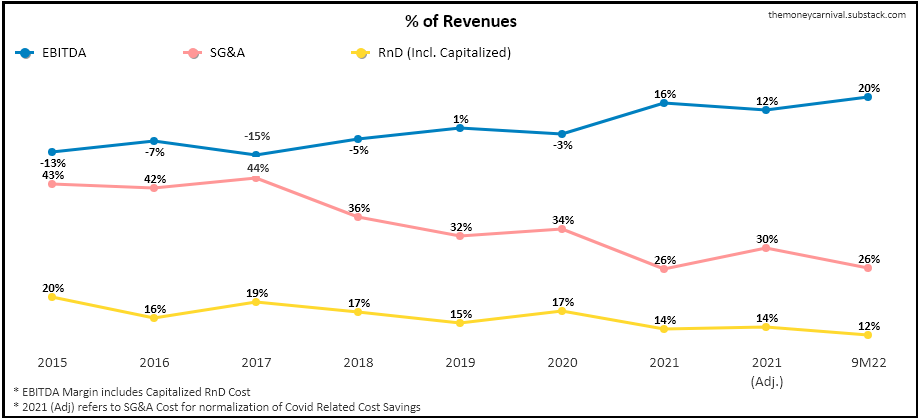

SG&A / RnD Expenses and Operating Margins

As revenues starts growing and company reaches a scale, it surpasses the growth of fixed expenses like sales and marketing, thus expanding the Margins over time.

SG&A costs has declined from 43% to 26% currently as a % of revenues. Even if we exclude Covid related cost savings (more detailed in Valuation Sheet) which should come about 62 Cr in 2021, we can see major decline in Costs and thus, expansion of EBITDA Margins.

Intellect has started capitalizing some part of RnD costs (for the products that are still in initial stages) from 4Q16, which we've included in below to calculate EBITDA Margin. Management guidance is to reach 30% EBITDA Margins (PnL Cost) in few quarters which should come about ~25% incl. Capitalized Expenses.

Part 4 : Management

Management plays a integral role when it comes to success of product companies. Building scalable profitable product business model needs long term vision and sharp focus. Arun Jain is the Founder and Promoter for Intellect. He build the company from having One Major Client (Citi Bank) under Polaris Services to Standalone separate Entity Intellect with currently 260+ clients including some of the Top leading banks in world.

There is a separate well defined organization structure and management for each product division will help in equal focus on all the products and less chances of disproportionate allocation of capital.

Newly formed 8 member strategic advisory board from diverse area of expertise

Management Guidance

Even though Intellect has shown good growth and margin improvement over the years, however, management has continuously failed to deliver numbers as per their guidance in given time periods. Due to this reason, the stock per se, has been quite volatile over the years. One of the reason for not achieving expected growth numbers could be volatile nature of license deals. It is really hard to predict volume of license deals for a given period which also impacts margins of the business. In next 4-5 years, as ratio of of SaaS + AMC revenues will increase, business will become more predictable.

Current Guidance for Business is 20% Revenue growth with 30%+ EBITDA margins. However, one should consider enough margin of safety on this guidance while doing valuations.

Part 5 : Growth Opportunities

Barriers to Entry

B2B products are really sticky in nature, each product has a high switching cost. Consider this, before buying a product, a company considers POCs from lot of vendors, then finalizes one product, spend resources for 1-2 years on implementation, UATs, training employees. There are generally two reasons to switch products, either drastic deterioration of quality of product or price gap with competitor becomes too huge to look reasonable.

For a product company, it generally takes time and capital to create product, finding market, deciding positioning and then another 2-3 years to reach a certain scale, which gives existing companies ample room to strengthen their position in market and hence, creating a consolidation in number of suppliers.

For Banking Products, knowledge of regulatory norms as per region and shaping product in that way is a technical know-how that creates another barrier for a new entrant to enter into market.

Operating Leverage x Business Tailwinds

Company has mentioned that desired product set is completed, so once these products starts getting monetized, there could be a chance of high operating leverage. Once products prove their effectiveness and reach enough scale, product companies can make high gross margins (60% +) and high operating margins (> 35%)

Strong Order Backlog and Consistent Increase in Deal Size in terms of number of deals and value of deals (more so, increasing LTV due to SaaS deals) gives comfort that they can sustain high teen Revenue growth numbers.

Cross Sell : 20% of active customers generated revenues from more than 1 Product.

Go-To Market Strategy

Horizontal Selling : Intellect's AI/ML tech and Magic Invoicing tech can have multiple use cases which can help them find market beyond BFSI.

Americas : $1bn addressable opportunity for Intellect in Americas in Hyperscale Corp Banking OS / Liquidity / Virtual Accounts / Escrow / Underwriting. Also, Data / Underwriting Products are getting acceptance among top 10 P&C Insurance Carriers with market of 150 P&C Insurers @$1m accounts.

Europe : Already strong reference for iGTB's Liquidity, Payments, Trade Finance. Expanding into Nordics Region. Lending, Underwriting, Wealth Management are set to expand in Europe in coming Quarters.

MEA : DTB is market leader in region. Top 8 of 9 banks are clients.

Payment, Lending, Digital Core, Underwriting are expected to reach critical mass in coming quarters.

Expecting to reach iRTM products up a scale in FY23

Optionality

Intellect is in process to start a dedicated AIF fund to invest in emerging fintech and tech companies to leverage their expertise in bagging better deals and improving product catalogue, a move towards building a ecosystem

Successful Product Companies are free cash flow machines, which don't need much larger incremental investments, hence Dividends / Buybacks are possibility here down the line

Part 6 : Vulnerabilities and Future Risks

Business Risks

As we already discussed, Missed Guidance is a risk factor which generally shakes the confidence of investors causing short / medium term volatility.

Except 4-5 Products, Other Products are yet to still reach a scale and any changes in technology can be a risk for their positioning in market

Company has DSO ~ 130 days currently out of which India Business has outstanding for 217 Days. Also, 30% of the receivables are based on milestones like Implementation and UATs. Any delay or failure in achieving milestones will cause risk to grow receivables. ~200Cr of Unbilled Revenues are from GeM segment because of nature of the contract where 70% of collection is done when buyer updates the sales order in system

Demand Risks

Moving to Digital and Buy vs Build has been a major driving force of high growth in lastcouple of years. Slowness in adoption rate can put pressure on growth and margins given multiple products are in investment phase and are being capitalized on balance sheet.

Success of product also depends to large extent on growth of end users. If banks and financial institutions can see better growth prospects, there'll be more chances to cross sell or up sell products.

Security and Integration Issues are also important factor for a Product Business, and even much more for Banking Products.

Part 7 : Valuation Model and Closing Thoughts

We’re adding google doc for valuation sheet for Intellect which should help you plug in your assumptions and track the company.

As per my analysis, company seems to be reasonably valued and downside seems to be low (currently), however, the stock is in momentum and has run up quite a lot in recent weeks. That being said, we could see dip in margins in some of recent quarters which can produce short term volatility giving better opportunities for consideration. This is based on my personal understanding and assumptions and my views could be biased or wrong.

It is an interesting opportunity in my opinion, worth analyzing and to keep an eye on. Let me know your take on valuations and business prospects.

Comment or connect on twitter for any feedback or queries regarding the business or valuation sheet. Feel free to make a copy of the file and edit assumptions to reach to your own conclusions.

If you’d like to learn more about Evaluating SaaS Business, check my previous post.

[Disclaimer: I'm not a SEBI Registered Investment or Financial Advisor. Any information in this article is from personal research and is not intended as, and shall not be understood or construed as , financial advice. It's very important to do your own analysis and reviewing the facts before making any investment based on your own personal circumstances. Kindly seek professional advice before taking investment decision.]

How did u arrive at 200cr Gem unbilled revenues